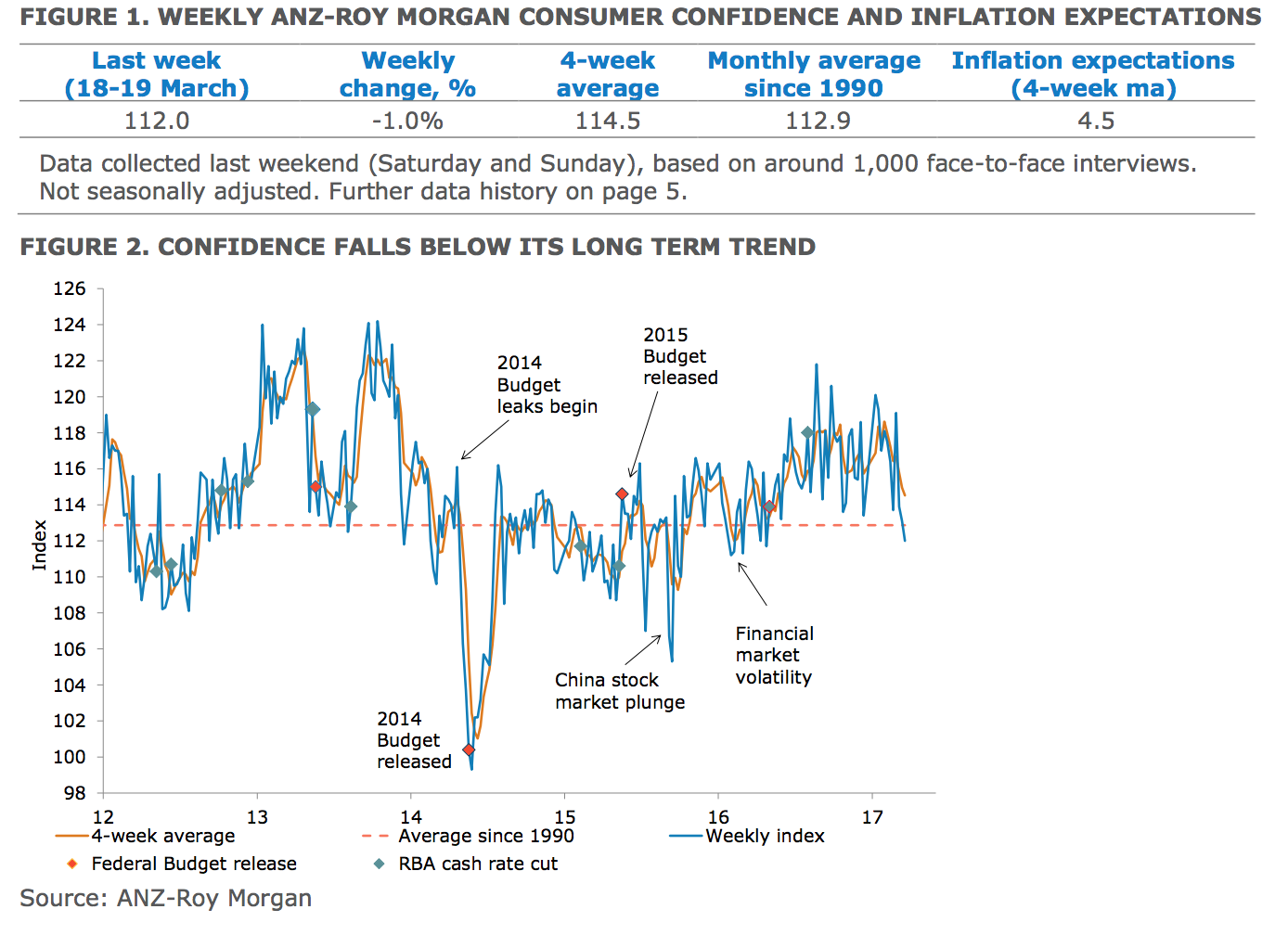

Consumer confidence: below average

Consumer confidence fell for the third straight week (down 1.0%), bringing the index to its lowest value since April 2016. The weakness in confidence was driven by households’ concerns about both current and future economic conditions.

Households’ views on the 12-month economic outlook fell 3.3% last week, after a sharp 5.2% fall the previous week. Consumers were also less confident regarding future economic conditions, with the sub index falling a solid 3.5% last week.

Households’ views towards their current finances improved 1.0%, while views towards future finances were broadly flat (down 0.1%). The future finances sub index is now at its lowest level since October 2016, although both sub-indices remain above their long term averages.

The ‘good time to buy a household item’ sub-index rose 0.4% last week following a 1.3% rise the previous week. This sub index is currently close to its long term trend.

The four week average for inflation expectations has stabilised around 4.5%, though this week’s reading has dropped to 4.1%.

ANZ’S HEAD OF AUSTRALIAN ECONOMICS DAVID PLANK COMMENTED:

“Confidence slipped for the third straight week, bringing the weekly number below its long term average for the first time since April 2016. The downward trend in confidence since late January is disappointing given the broadly supportive economic conditions – the solid Q4 GDP report, an improving current account, strong housing market and above trend business conditions.

In our view, concerns about labour market conditions have likely weighed on confidence over the past few weeks. Continued soft wages growth is likely a factor and last week’s reported rise in the unemployment rate for February may have weakened confidence, not least by further dampening income expectations. Despite decent strength on the activity side of the economy, low wage growth remains a key downside risk to both the inflation and spending outlook over 2017, in our view.”